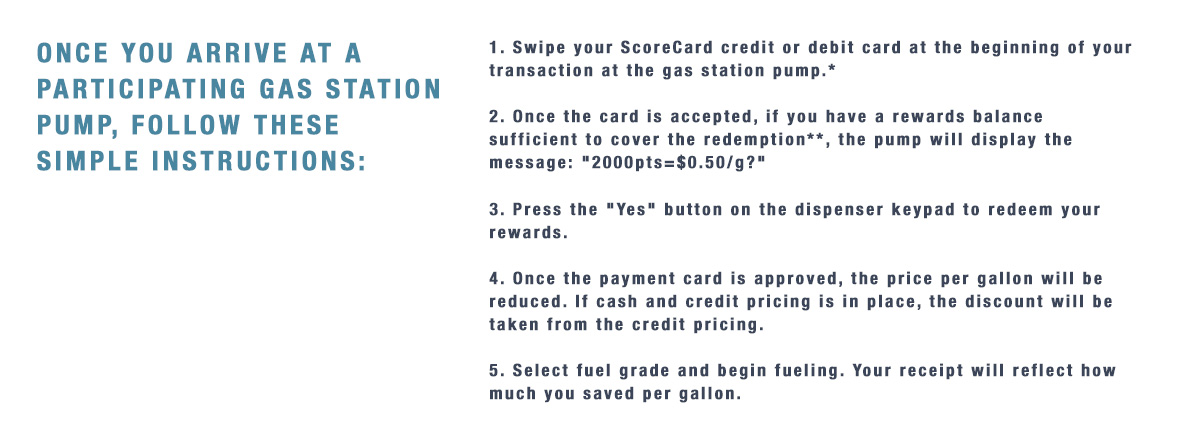

9 Research-Backed Habits Of Happy People

Are you thriving? Struggling? Or suffering? Those are the three ways global analytics and advice firm Gallup classifies people. And at the moment, according to Its polls, the number of Americans thriving has dropped to lows not seen since the 2008 economic downturn. The poll also found the amount of stress and worry people feel on a daily basis hasn’t fully dropped to pre-pandemic levels.

Gallup’s data is worth considering. However, what it means to “thrive” is subjective. Some would say thriving is a mindset and being happy doesn’t come from having a lot, but rather from being grateful for what you have. That’s not to say there isn’t value in always striving for more. But if you’ve decided, “I’ll only be happy when [insert goal here],” you could be missing out on a lot of joy that’s available right now.

It is worth acknowledging that some of our happiness levels are genetic. In fact, a chart published in Berkeley University’s Greater Good Magazine shows 50 percent of joy is in your genes. But it also reports that 40 percent of your happiness relies on your behaviors and habits – so a lot is actually within your control. Based on a data, research and surveys, here are the habits of happy people.

They Exercise

Source: kali9 / Getty

You don’t need to engage in a serious sweat session every day to feel happy. But you should be pumping some iron on a regular basis. Many studies have linked regular exercise to happiness. And one such study published in the International Journal of Environmental Research and Public Health showed this to be true for young, middle-aged and older adults. In examining 2,345 healthy adults, it was discovered that regular physical activity was linked to greater feelings of happiness and life satisfaction.

They Go Outside

Source: Alistair Berg / Getty

Getting outdoors on a regular basis can significantly improve happiness levels. The American Psychology Association states that time in nature can lower stress, increase feelings of empathy and even improve attention span. Simply looking at natural landscapes from trees and rivers to mountains can achieve this effect. So if you pair time outdoors with your workout, you get double the benefits.

They Are Generous

Source: SDI Productions / Getty

It turns out that being happy isn’t about what you get, but rather what you give. Generous people are some of the happiest. In Adam Grant’s book Give and Take, it is reported that volunteers are some of the happiest people in the world. One study covered in the book found that volunteering increased happiness and self-esteem. Some studies even found that elderly adults who volunteer live longer.

Source: Xavier Lorenzo / Getty

Many spiritual gurus and psychology experts would tell you that happiness is simply the feeling of gratitude for the things that you have. All of the riches in the world can’t make you feel happy if you don’t feel grateful for them. Research published in Harvard Health Publishing showed a significant correlation between expressing gratitude and feeling joy.

They Forgive

Source: Westend61 / Getty

According to the American Psychological Association, being forgiving can help alleviate anxiety and symptoms of depression. It can even reduce the likelihood of some psychiatric disorders. So if you’re holding onto any grudges, the only person you could be harming is you.

Research also shows that forgiving yourself is an important part of the happiness equation. A study published in the journal Human Development found that self-compassion is linked to happiness, optimism and feeling connected to others. It’s also linked to decreased depression, anxiety and fear.

They Plan Things

Source: Olelole / Getty

Happy people have active, busy lives full of things that they look forward to from hobbies and socializing to trips. According to research from the Applied Research in Quality of Life, also shared in the Huffington Post, the simple act of planning a trip elevates happiness levels. So you get to be happy twice when you make a plan: first when you set it in motion, and then when you actually do the plan. It’s no wonder this is one of the more common habits of happy people.

They Devote Time To Loved Ones

Source: tomazl / Getty

If you think happiness is on the other side of career success, think again. Martin Seligman, a known psychologist who has long studied the habits of happy people, reports in his book Authentic Happiness – based on his website – that people who are “very happy” spend the least amount of time alone and have rich social lives.

They Meditate

Source: Geber86 / Getty

Research published in the journal Personality and Individual Differences found a strong correlation between frequent meditation and high happiness levels. So while there is a joy to be found in planning things and looking forward to the future, there is also joy in being present right where you are.

They Value Experiences Over Things

Source: Dimensions / Getty

The American Psychological Association reports that valuing materialistic objects is linked to higher levels of depression, anxiety, and health issues like stomachaches and headaches. It’s something psychotherapist Richard Wiseman discusses in his book 59 Seconds, too. He notes that spending money on experiences over products contributes to both long and short-term happiness.